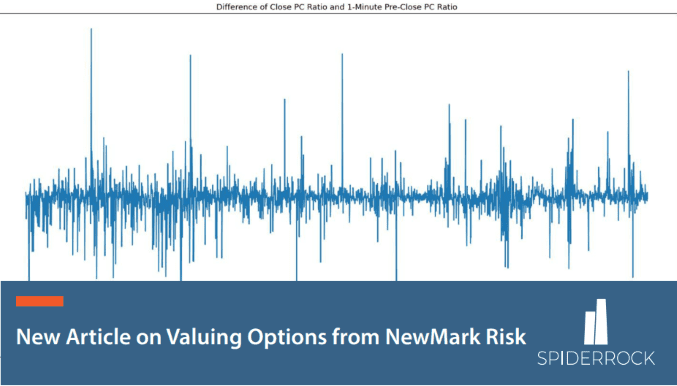

NewMark Risk has recently released an article on valuing options. In the article, NewMark provides practical differences in pricing options and their impact. The article examines two signals, Put-Call Volume Ratio and IV Spread, using data from both SpiderRock and EDI. The results of the signals from both datasets can be seen in the image below.

As this article shows, SpiderRock’s Options Close Mark dataset can be used to value options and create different signals. For more, read the article here: NewMarkRisk – Options Derived Analytics | NewMarkRisk